Confirmed Steps For The Qualified Dividends And Capital Gains Tax Worksheet Don't Miss! - Sebrae MG Challenge Access

Behind every investor’s confident tax filing lies a quiet, intricate ledger—one that demands precision, not luck. The Qualified Dividends and Capital Gains Tax Worksheet is far more than a spreadsheet; it’s the financial equivalent of a surgeon’s scalpel, enabling investors to navigate the nuanced terrain of tax implications with surgical accuracy. For decades, savvy investors have relied on this tool not just to comply, but to optimize—yet few truly understand its hidden mechanics.

Understanding the Taxonomy: Qualified vs.

Understanding the Context

Non-Qualified Streams

At its core, the worksheet separates two distinct tax categories: qualified and non-qualified dividends and gains. Qualified dividends—typically from U.S. corporations or certain foreign entities—are taxed at preferential long-term rates, often capped at 20% under current U.S. policy.

Image Gallery

Recommended for you

Recommended for you

Key Insights

Non-qualified dividends and short-term capital gains, in contrast, face ordinary income tax rates that can climb to 37%, depending on filers’ income brackets. But here’s the twist: not all income flows through the same channel. A single stock transaction can generate both types, demanding granular tracking. First-time investors often overlook this bifurcation, leading to overpayment or surprises come tax season.

Mapping the Worksheet: Core Components and Calculations

The worksheet begins with income source identification—dividends declared, capital gains from asset sales, and holding period durations. Each transaction must be logged with precision: date of purchase, sale price, adjusted cost basis, and holding period.

Related Articles You Might Like:

Finally Evasive Maneuvers NYT Warns: The Danger You Didn't See Coming! Real Life

Urgent Nashville’s February climate: a rare blend of spring warmth and seasonal transitions Must Watch!

Busted Los Angeles Times Crossword Solution Today: The Answer That's Breaking The Internet. Must Watch!

Final Thoughts

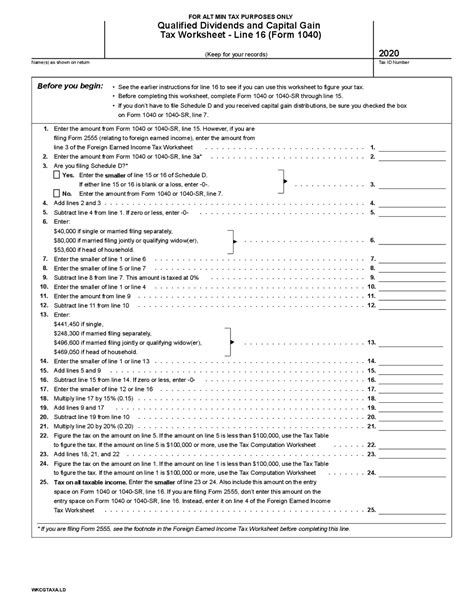

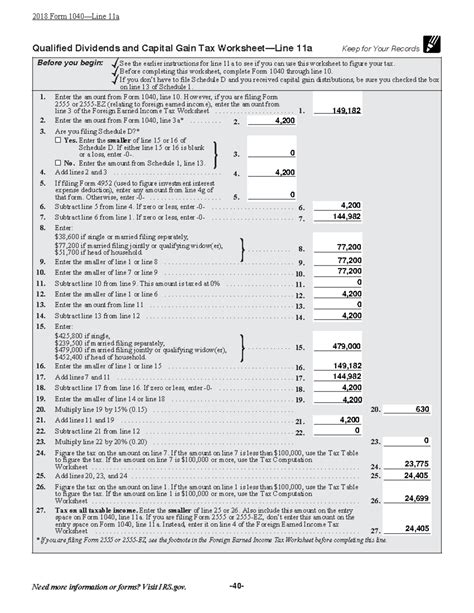

For qualified dividends, the critical threshold is the holding period: dividends from shares held over 61 days qualify; those held shorter trigger non-qualified treatment. But here’s where complexity emerges: qualified dividends from securities held over five years benefit from the 20% rate, yet this advantage vanishes if the holding period is breached. The worksheet must flag such risk zones explicitly. Capital gains calculations introduce another layer: short-term gains (held under one year) are taxed as ordinary income, while long-term gains (over one year) qualify for preferential treatment. Misclassifying a holding period can distort effective tax rates by double digits—enough to erode portfolio returns.

Key fields demand rigorous attention. The adjusted basis, calculated as purchase price minus inflation adjustments and prior distributions, is the worksheet’s foundation.

Understanding the Context

Non-Qualified Streams

At its core, the worksheet separates two distinct tax categories: qualified and non-qualified dividends and gains. Qualified dividends—typically from U.S. corporations or certain foreign entities—are taxed at preferential long-term rates, often capped at 20% under current U.S. policy.

Image Gallery

Key Insights

Non-qualified dividends and short-term capital gains, in contrast, face ordinary income tax rates that can climb to 37%, depending on filers’ income brackets. But here’s the twist: not all income flows through the same channel. A single stock transaction can generate both types, demanding granular tracking. First-time investors often overlook this bifurcation, leading to overpayment or surprises come tax season.

Mapping the Worksheet: Core Components and Calculations

The worksheet begins with income source identification—dividends declared, capital gains from asset sales, and holding period durations. Each transaction must be logged with precision: date of purchase, sale price, adjusted cost basis, and holding period.

Related Articles You Might Like:

Finally Evasive Maneuvers NYT Warns: The Danger You Didn't See Coming! Real Life Urgent Nashville’s February climate: a rare blend of spring warmth and seasonal transitions Must Watch! Busted Los Angeles Times Crossword Solution Today: The Answer That's Breaking The Internet. Must Watch!Final Thoughts

For qualified dividends, the critical threshold is the holding period: dividends from shares held over 61 days qualify; those held shorter trigger non-qualified treatment. But here’s where complexity emerges: qualified dividends from securities held over five years benefit from the 20% rate, yet this advantage vanishes if the holding period is breached. The worksheet must flag such risk zones explicitly. Capital gains calculations introduce another layer: short-term gains (held under one year) are taxed as ordinary income, while long-term gains (over one year) qualify for preferential treatment. Misclassifying a holding period can distort effective tax rates by double digits—enough to erode portfolio returns.

Key fields demand rigorous attention. The adjusted basis, calculated as purchase price minus inflation adjustments and prior distributions, is the worksheet’s foundation.

Without it, gains inflate and taxes balloon. Equally vital is the holding period counter—automated systems often fail here, especially with fractional shares or portfolio rebalancing. A single misrecorded day can invalidate the entire tax position, exposing investors to penalties or audits. The best worksheets integrate audit trails: timestamped entries, source document links, and reconciliation checks that mirror internal control standards.

Step-by-Step Execution: Building the Worksheet with Confidence

First, consolidate transaction data from brokerage statements, 1099s, and tax software exports.