Urgent Explanation Of 501c4 And 5 Political Activity For Beginners Don't Miss! - Sebrae MG Challenge Access

At first glance, 501(c)(4) and 501(c)(5) nonprofit statuses appear as technical footnotes in tax law—abstract classifications mostly relevant to accountants and compliance officers. But dig deeper, and you uncover a dynamic battleground where organizations shape public discourse, influence policy, and operate in a gray zone between advocacy and accountability. For newcomers, understanding these designations isn’t just about tax codes—it’s about navigating the mechanics of civic power.

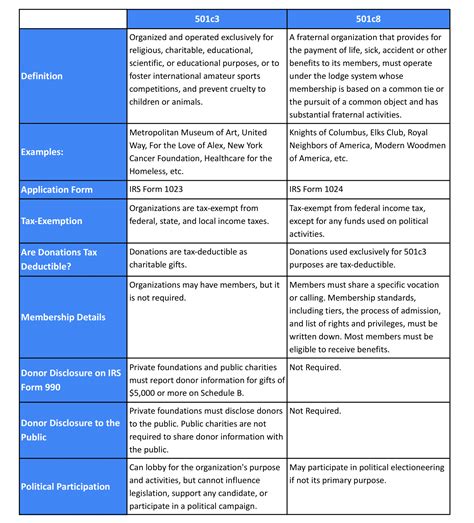

Unpacking the Labels: 501(c)(4) vs.

Understanding the Context

501(c)(5)—Definitions and Distinctions

501(c)(4) entities are social welfare organizations designed to promote community well-being, with a critical caveat: while they may engage in limited political activity, their primary purpose must serve a broader social benefit. The IRS mandates that political influence remains incidental, not core. In contrast, 501(c)(5) groups are explicitly labor, agricultural, or commercial interest associations, legally permitted to advocate more aggressively on policy matters—so long as their advocacy aligns with their core mission. This distinction isn’t just semantic; it defines operational boundaries and public perception.

Beginners often overlook the hidden mechanics: political activity isn’t a binary.

Image Gallery

Recommended for you

Recommended for you

Key Insights

It spans from behind-the-scenes lobbying and issue ads to direct voter mobilization—each carrying different compliance risks. A 2023 study by the Center for Responsive Politics found that 501(c)(4)s now lead in election-related spending, outpacing traditional PACs in dark money contributions. Why? Because they exploit loopholes in disclosure rules—often shielded by vague “social welfare” claims.

How Political Activity Is Permitted—and Exploited

501(c)(4)s can participate in lobbying, running advocacy campaigns, and even funding independent expenditures—provided such efforts don’t become their primary function. But here’s the twist: when activity crosses the threshold into “substantial” political campaigning, the line blurs.

Related Articles You Might Like:

Urgent This Guide To Rural Municipality Of St Andrews Shows All Laws Act Fast

Verified Husqvarna Push Mower Won't Start? I'm Never Buying One Again After THIS. Watch Now!

Revealed Peltor Leads With Refined Ear Protection For Relentless Environments Hurry!

Final Thoughts

Take union-backed 501(c)(5) groups, for example. These labor-aligned organizations can endorse candidates and push for policy changes, but only if their core business—representing workers—remains intact. A 2022 case involving a major union’s 501(c)(5) arm revealed how quickly advocacy can morph into electoral intervention, drawing scrutiny from both regulators and the public.

What’s often missed is the financial architecture. The IRS requires 501(c)(4)s to file Form 990, but political activity disclosures are selective. Some groups obscure spending by categorizing it as “educational” or “community outreach,” effectively laundering funds toward political ends. This opacity fuels skepticism—especially when 501(c)(4)s now control over $10 billion in untraceable political spending, according to OpenSecrets.

Understanding the Context

501(c)(5)—Definitions and Distinctions

501(c)(4) entities are social welfare organizations designed to promote community well-being, with a critical caveat: while they may engage in limited political activity, their primary purpose must serve a broader social benefit. The IRS mandates that political influence remains incidental, not core. In contrast, 501(c)(5) groups are explicitly labor, agricultural, or commercial interest associations, legally permitted to advocate more aggressively on policy matters—so long as their advocacy aligns with their core mission. This distinction isn’t just semantic; it defines operational boundaries and public perception.

Beginners often overlook the hidden mechanics: political activity isn’t a binary.

Image Gallery

Key Insights

It spans from behind-the-scenes lobbying and issue ads to direct voter mobilization—each carrying different compliance risks. A 2023 study by the Center for Responsive Politics found that 501(c)(4)s now lead in election-related spending, outpacing traditional PACs in dark money contributions. Why? Because they exploit loopholes in disclosure rules—often shielded by vague “social welfare” claims.

How Political Activity Is Permitted—and Exploited

501(c)(4)s can participate in lobbying, running advocacy campaigns, and even funding independent expenditures—provided such efforts don’t become their primary function. But here’s the twist: when activity crosses the threshold into “substantial” political campaigning, the line blurs.

Related Articles You Might Like:

Urgent This Guide To Rural Municipality Of St Andrews Shows All Laws Act Fast Verified Husqvarna Push Mower Won't Start? I'm Never Buying One Again After THIS. Watch Now! Revealed Peltor Leads With Refined Ear Protection For Relentless Environments Hurry!Final Thoughts

Take union-backed 501(c)(5) groups, for example. These labor-aligned organizations can endorse candidates and push for policy changes, but only if their core business—representing workers—remains intact. A 2022 case involving a major union’s 501(c)(5) arm revealed how quickly advocacy can morph into electoral intervention, drawing scrutiny from both regulators and the public.

What’s often missed is the financial architecture. The IRS requires 501(c)(4)s to file Form 990, but political activity disclosures are selective. Some groups obscure spending by categorizing it as “educational” or “community outreach,” effectively laundering funds toward political ends. This opacity fuels skepticism—especially when 501(c)(4)s now control over $10 billion in untraceable political spending, according to OpenSecrets.

It’s not just about money; it’s about influence without transparency.

Why It Matters: The Hidden Mechanics of Influence

Political activity under 501(c)(4) and 501(c)(5) isn’t just a legal exercise—it’s a strategic lever. These entities amplify niche voices, shape public opinion through targeted messaging, and pressure lawmakers with grassroots campaigns. Yet their power rests on asymmetry: they benefit from nonprofit tax status while wielding disproportionate sway. For beginners, the challenge is recognizing that compliance doesn’t equate to ethics.